Understanding Inflation: A Beginner’s Guide

Inflation is often seen as a necessary economic phenomenon that affects much of the daily lives of individuals and businesses. It signifies an increase in the price levels of goods and services within an economy over a period of time. Understanding inflation requires exploring its causes, effects, and implications on personal finances and the economy overall. Inflation can result from various factors, including increased production costs, rising demand for products, or expansive monetary policies by governments. Consumers might notice their purchasing power decrease as inflation affects the cost of living. When prices rise, the same amount of money can buy fewer goods, influencing living standards significantly. Furthermore, inflation affects interests rates, investment strategies, and savings. Consumer behavior can also change, leading to impacts on spending habits and economic growth. Monitoring inflation rates is crucial for making informed financial decisions, as it influences interest rates and returns on investments. Understanding how inflation works helps individuals manage their personal finances, negotiate salaries, and plan for retirement. Awareness of inflation is crucial in ensuring financial stability in an often volatile economy.

Causes of Inflation

The causes of inflation can be broadly categorized into demand-pull inflation and cost-push inflation. Demand-pull inflation occurs when the demand for goods and services exceeds supply, prompting businesses to raise prices. It often coincides with economic growth, increased consumer spending, or lower interest rates, which stimulate borrowing and spending. For instance, during times of rapid economic growth, the surge in consumer demand can lead to inflationary pressures. Conversely, cost-push inflation arises when production costs increase, such as rising wages or material prices. This type of inflation can occur regardless of demand. For example, if oil prices surge, transportation and manufacturing costs can escalate, leading businesses to pass those costs onto consumers. External factors, like trade policies or geopolitical tensions, can also affect supply chains, increasing prices. Governments and central banks often monitor inflation closely to implement policies aimed at controlling it. By adjusting interest rates or utilizing monetary policies, these institutions seek to balance economic growth with price stability, ensuring that inflation remains within acceptable limits. Individuals should understand these factors, as inflation affects purchasing power and long-term financial planning significantly.

Inflation impacts different sectors of the economy in diverse ways, affecting wages, investments, and asset values. As inflation rises, employers may feel pressure to increase wages to keep pace with rising living costs. However, companies might struggle to raise salaries at the same rate, which can result in a reduction in employee satisfaction and productivity. In contrast, certain investments, like stocks and real estate, often perform better during inflationary periods, as companies can increase their prices and potentially grow profits. Though real estate might appreciate due to increased demand, fixed-income investors may find their returns diminished as inflation erodes the purchasing power of their interest payments. Inflation can also negatively affect savings, especially in traditional savings accounts that offer low interest rates. Individuals who do not invest their savings adequately may lose out over time. Thus, understanding the implications of inflation on various sectors can empower individuals to make educated investment decisions and protect their assets from erosion. It is essential to adapt financial strategies considering the ongoing economic conditions and how inflation might evolve in the future.

Understanding Deflation

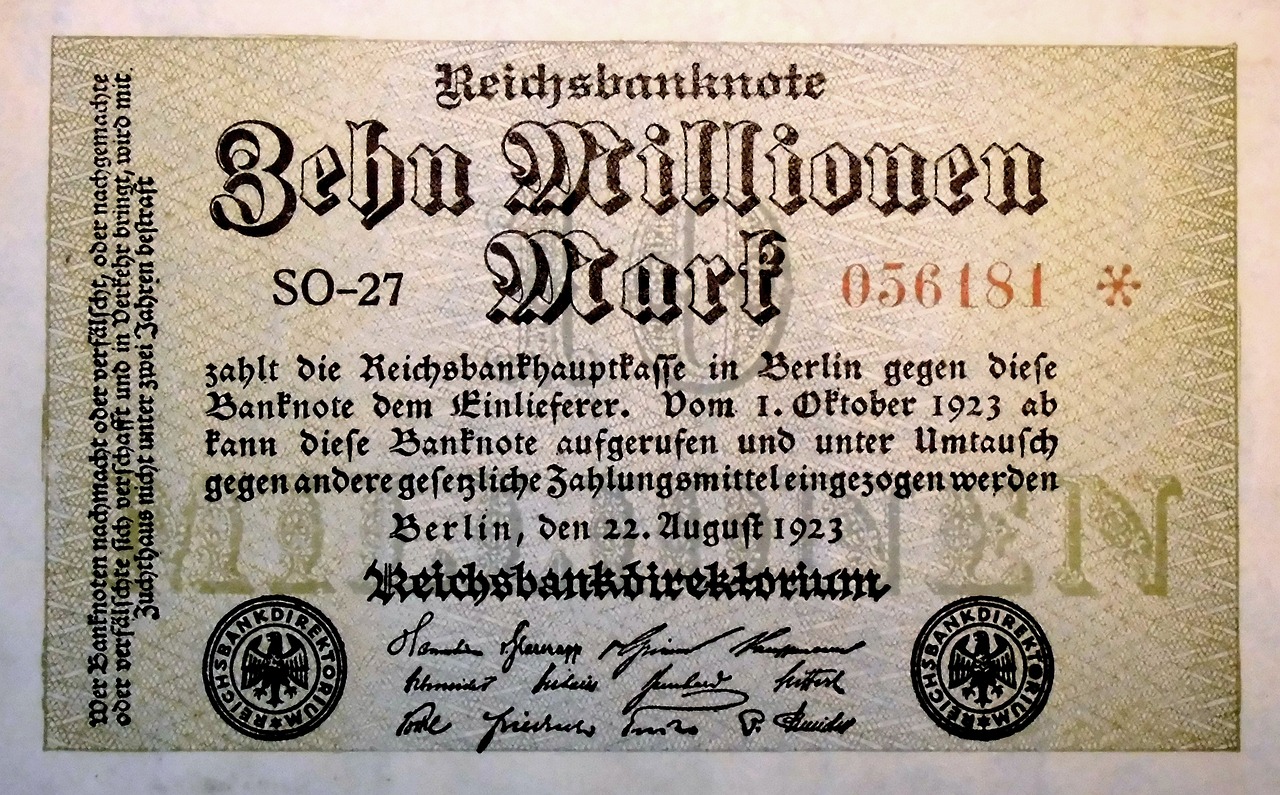

Deflation is the opposite of inflation, characterized by a decline in the general price level of goods and services. While inflation indicates rising prices, deflation portrays falling prices, often linked with decreased consumer demand and economic stagnation. When prices drop, it can lead to a vicious cycle affecting wages, spending, and investment. Consumers may delay purchases, anticipating even lower prices, thereby decreasing overall demand and further exacerbating deflation. This hesitancy can hinder economic growth, lead to layoffs, and increase unemployment rates. Deflation can also encourage companies to cut their prices to compete effectively, resulting in lower profit margins. The phenomenon is particularly concerning for borrowers, as the real value of debt increases in a deflationary environment. As a result, businesses and individuals may find it challenging to repay loans. Central banks often respond to deflation by implementing measures to stimulate the economy, such as lowering interest rates or enacting quantitative easing. Understanding deflation’s causes and effects is essential for individuals to navigate financial challenges and adapt their financial strategies accordingly while maintaining awareness of the economic landscape.

The relationship between inflation, deflation, and interest rates plays a crucial role in personal finance management. Central banks, such as the Federal Reserve, utilize interest rate policies as tools to combat inflation and deflation. When inflation rates rise above target levels, central banks typically increase interest rates to slow down economic activity, ultimately reducing inflationary pressures. Conversely, during periods of deflation, central banks might lower interest rates to stimulate spending and investment, encouraging economic growth. Rates directly impact borrowing costs, affecting mortgages, credit cards, and loans. Higher interest rates can discourage borrowing and spending, which in turn can lead to slower economic growth, while lower rates generally incentivize borrowing, thus supporting personal purchases and investments. Individuals should stay informed about prevailing interest rates and their relationship to inflation and deflation, as this knowledge can guide crucial financial decisions. Understanding how interest rates fluctuate in response to inflation and deflation can empower consumers to make savvy financial choices while managing debt, investments, and overall financial well-being in varying economic conditions.

Inflation’s Impact on Savings and Investments

Inflation significantly affects savings and investments, with long-term implications for financial security. Traditional savings accounts often yield low-interest rates, which do not keep pace with rising inflation rates. As inflation erodes purchasing power, individuals might find their savings losing value over time. For example, if the inflation rate surpasses the interest earned on a savings account, savers effectively lose money. This reality highlights the importance of investing in assets that appreciate over time, such as stocks, real estate, or commodities. Equities tend to perform well during inflationary periods, as companies increase prices in response to rising costs, potentially leading to higher profits and stock appreciation. Real estate often appreciates in value over time, making it a reliable hedge against inflation. Alternatively, fixed-income investments, like bonds, may see their value decrease as inflation rises. Consequently, understanding asset allocation and investment diversification is essential to combat inflation’s effects on savings effectively. By adopting strategies to mitigate risks associated with inflation, individuals can safeguard their financial future and maintain purchasing power in an evolving economic landscape.

In conclusion, understanding inflation and deflation is essential for everyone navigating the economic landscape. By grasping the nuances of these phenomena, individuals can make informed financial decisions that preserve their purchasing power and promote financial stability. Monitoring inflation rates, understanding the causes and effects, and adapting financial strategies accordingly are all critical components of effective personal finance management. Being proactive in investment choices and staying informed about interest rate changes can further enhance one’s financial resilience. Additionally, understanding how inflation and deflation impact various aspects of life, from wages to savings, can empower individuals to navigate challenges with a more strategic mindset. It is vital to adopt a long-term perspective in financial planning, considering how economic variables can influence investment returns and purchasing power over time. Through comprehensive financial education and awareness of inflation’s intricacies, individuals can better prepare for unforeseen economic shifts. Ultimately, fostering a deep understanding of these economic concepts will create a foundation for long-term financial well-being, allowing people to thrive in a world marked by constant economic change.

In conclusion, understanding inflation and deflation is essential for everyone navigating the economic landscape. By grasping the nuances of these phenomena, individuals can make informed financial decisions that preserve their purchasing power and promote financial stability. Monitoring inflation rates, understanding the causes and effects, and adapting financial strategies accordingly are all critical components of effective personal finance management. Being proactive in investment choices and staying informed about interest rate changes can further enhance one’s financial resilience. Additionally, understanding how inflation and deflation impact various aspects of life, from wages to savings, can empower individuals to navigate challenges with a more strategic mindset. It is vital to adopt a long-term perspective in financial planning, considering how economic variables can influence investment returns and purchasing power over time. Through comprehensive financial education and awareness of inflation’s intricacies, individuals can better prepare for unforeseen economic shifts. Ultimately, fostering a deep understanding of these economic concepts will create a foundation for long-term financial well-being, allowing people to thrive in a world marked by constant economic change.