Digital Payment Solutions for Microfinance Repayments

Microfinance institutions play a significant role in promoting financial inclusion, especially in developing economies. The introduction of digital payment solutions is revolutionizing the way clients make repayments. With the advent of smartphones and the internet, microfinance clients can easily access online platforms that facilitate repayments. Electronic payment systems offer numerous advantages when compared to traditional cash transactions. Digital transactions enhance transparency and tracking, reducing the risks associated with cash handling. Additionally, these systems often come with lower transaction fees, making them a more cost-effective option for both clients and lenders. Furthermore, clients can repay their loans at their convenience, eliminating the need to travel long distances to physical branches. This convenience can significantly improve the repayment rates of microfinance institutions because clients appreciate the accessibility and speed these systems provide. To leverage these advantages, microfinance institutions need to conduct proper training sessions for their clients. By ensuring users are comfortable with digital payment methods, it’s possible to achieve higher satisfaction rates and foster a culture of prompt repayments in microfinance.

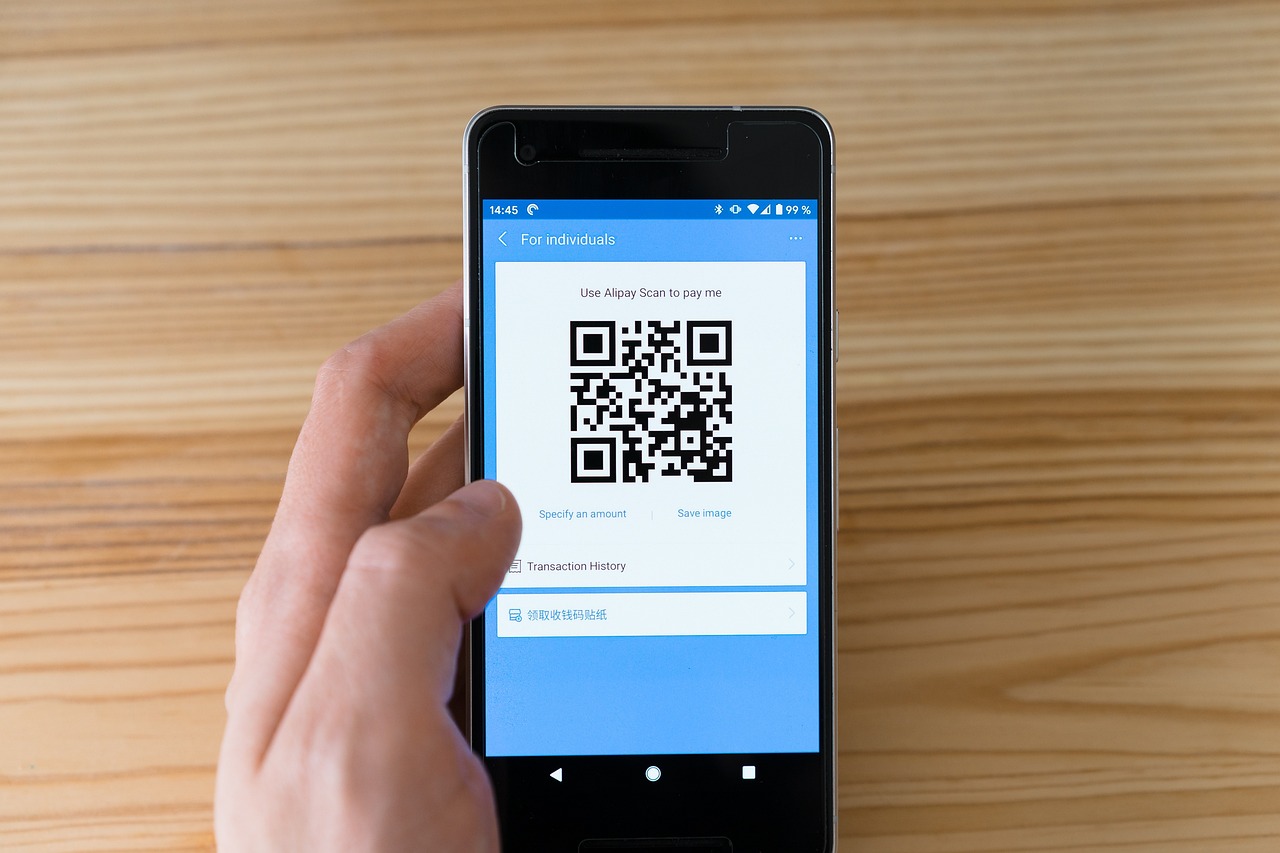

Moreover, integrating mobile wallet applications into the repayment process can significantly enhance user experience. Mobile wallets enable clients to store funds and pay bills with just a few taps on their smartphones. These platforms often involve partnerships with local telecom providers to facilitate seamless transactions. Additionally, many mobile wallets offer sign-up bonuses or rewards for frequent usage, incentivizing clients to adopt digital payments. Over time, clients become accustomed to these technologies, easing the transition from traditional methods to digital solutions. Security is a pivotal concern in adopting digital payments for microfinance. To mitigate this, it is crucial to educate clients on safe transaction practices, including using secure passwords and avoiding suspicious links. Moreover, institutions need to employ robust encryption technologies to protect sensitive information. Any breaches can significantly damage trust between the institution and its clients. By fostering secure digital transactions, microfinance institutions can build a foundation of trust. Overall, mobile wallets offer an effective alternative to cash repayments, driving efficiency and improving financial management for clients within the microfinance space.

Benefits of Digital Payment Solutions

One essential benefit of digital payments in microfinance is the speed of transaction processing. Traditional repayment methods often involve delays due to manual handling of cash. Digital transactions, on the other hand, can be processed almost instantly. Clients appreciate the speed, which leads to higher satisfaction and faster loan disbursement cycles for institutions. Moreover, the automated nature of digital payments reduces human errors that often occur in manual processes. These errors can lead to discrepancies, delays, and client dissatisfaction. By automating repayments, microfinance institutions can not only enhance accuracy but also minimize administrative costs. Another critical advantage is the ability to gather data for better decision-making. Digital transactions leave behind a digital footprint, allowing institutions to analyze repayment patterns effectively. This data-driven approach enables microfinance institutions to tailor their services to client needs. For instance, understanding when clients most often make repayments can help institutions create flexible schedules or additional features that resonate with their clients. Data analysis fosters innovation and supports continuous improvement in service delivery, which is crucial for sustainability in the microfinance sector.

However, challenges still exist in deploying these digital payment solutions. Digital literacy remains a significant barrier for many clients, particularly in rural or underserved areas. To effectively implement digital solutions, microfinance institutions must prioritize education and training initiatives. Providing clients with hands-on training sessions can boost confidence in their digital payment abilities. Institutions can also create user-friendly resources, such as video tutorials or easy-to-follow guides. This approach demystifies the technology, ensuring that all clients, regardless of their educational background, feel empowered to participate. Additionally, collaboration with local communities can enhance the adoption of digital payments. Engaging with community leaders and influencers can facilitate acceptance and create a supportive environment for learning. This grassroot approach is key to ensuring that clients feel comfortable and informed. Ultimately, fostering an inclusive atmosphere around digital payments benefits everyone involved. When all parties work collaboratively towards a common goal, greater financial inclusion can be achieved through microfinance. This inclusiveness is vital for overcoming barriers to digital payment adoption.

Future Outlook for Digital Payments

The future of digital payment solutions in microfinance looks promising as technology continues to evolve. Many anticipate that blockchain technology will play a crucial role in enhancing transaction security and transparency. By utilizing distributed ledgers, microfinance institutions can provide clients with an unalterable record of their transactions. This transparency builds trust and accountability, which are essential in maintaining successful client relationships. Furthermore, the potential for integrating artificial intelligence (AI) into repayment processes opens up new opportunities. AI can facilitate personalized financial advice, assisting clients in managing their repayments more effectively. Additionally, AI tools can help institutions in risk assessment, identifying potential repayment issues before they escalate. Predictive analytics will provide invaluable insights into client behavior, allowing institutions to offer tailored support. However, the successful integration of these advanced tools requires an ongoing commitment to client education and a willingness to adapt to changing technology. By embracing innovation, microfinance institutions can not only enhance their repayment processes but also significantly improve the overall experience for their clients, driving the future of microfinance forward.

Despite the potential advancements, resistance to change often hinders the implementation of digital solutions. Many clients may retain a strong preference for cash transactions due to familiarity or security concerns. To overcome this, microfinance institutions must adopt a gradual approach to digital payment integration. Introducing hybrid models that allow clients to choose their preferred payment methods initially can boost acceptance. Over time, clients may become more comfortable with digital options as they witness their convenience and efficiency. Consistent feedback from clients about their experiences can facilitate ongoing improvements in technology adoption strategies. Engaging clients in discussions about their preferences and concerns can also foster loyalty and trust. Marketing initiatives highlighting success stories of clients who have transitioned to digital payments can serve as effective motivation for others. A focus on clear communication ensures that clients fully understand the benefits of digital solutions, ultimately driving broader acceptance. Thus, a balanced approach to integrating technology with traditional methods reinforces the long-term success of microfinance initiatives in the digital age.

Conclusion: Embracing Digital Solutions in Microfinance

Embracing digital payment solutions in microfinance is essential for promoting financial inclusion and empowering underserved individuals. The numerous benefits, such as speed, accuracy, and data-driven insights, highlight the importance of transitioning to digital platforms. By prioritizing education and community engagement, microfinance institutions can address existing barriers and foster an inclusive financial ecosystem. The future outlook appears bright, with advanced technologies set to revolutionize repayment processes further. However, overcoming resistance to change remains a significant challenge that institutions must navigate thoughtfully. Implementing hybrid solutions initially can ease clients into digital payments, paving the way for broader adoption. Continuous feedback loops and success stories can encourage a positive outlook among clients. Moreover, establishing a culture of trust around digital transactions is crucial. Institutions must be transparent about security measures and prioritize client education. Overall, the successful integration of digital payments not only enhances repayment efficiency but also drives institutional growth. As microfinance institutions evolve alongside technology, they can fulfill their mission of creating economic opportunities for all, ultimately leading to sustainable development in communities worldwide.

The continuous evolution of these digital solutions must remain a priority for institutions. Regular assessments of technology performance, client satisfaction levels, and evolving trends will help stakeholders stay informed. By fostering a culture of innovation, microfinance institutions can adapt to the financial needs of their clients effectively. Investing in research and development will ultimately lead to the creation of user-centric products and services tailored for each client. Therefore, embedding a strategy for ongoing improvement within the institutional framework is crucial for sustaining the positive trajectory of microfinance and ensuring that it continues to meet the growing demands of its clients. As the global landscape shifts towards digital financial solutions, microfinance remains pivotal in promoting equitable access to resources. Institutions must remain vigilant, embrace change, and lead the way for their clients into a digitally inclusive future. By championing financial literacy and technology adoption, microfinance can build stronger and more resilient communities. This proactive approach will create lasting relationships with clients and enhance the overall impact of microfinance in empowering those who are often left behind financially.