Digital Wallets and Their Influence on Banking Transactions

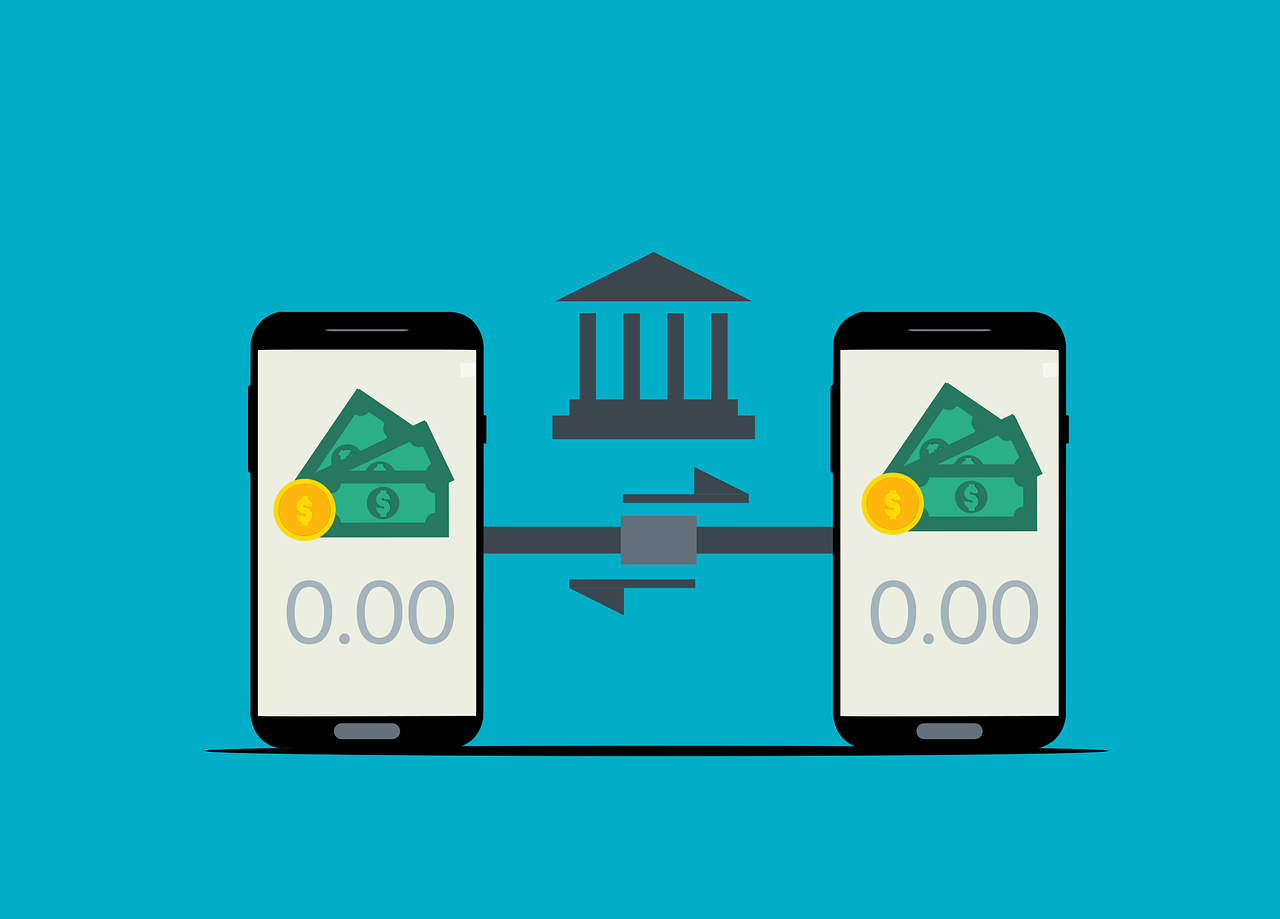

Digital wallets have revolutionized the way people manage their finances today, providing a seamless experience for transactions. As financial technology advances, these wallets become essential for consumers and businesses alike, making banking more convenient. Users can store their information securely in these digital platforms, allowing quick access to funds without carrying physical cash. This increase in efficiency means that transactions can occur in real time, whether online or in storefronts. Moreover, digital wallets often come with additional features, such as built-in budgeting tools and spending analytics, which help consumers stay on top of their expenses. Banking institutions have embraced this technology, integrating digital wallet solutions into their services. Additionally, the competitive landscape of financial services has prompted banks to innovate continuously, ensuring that they keep up with customer preferences. Digital wallets attract both tech-savvy millennials and more traditional consumers, enhancing user engagement. Notably, security remains paramount in the adoption of these technologies, pushing firms to implement robust security measures, including biometric authentication. Overall, the influence of digital wallets on banking transactions is undeniable and continues to reshape the financial sector.

The growth of mobile payments has spurred significant transformations in banking interactions. As more individuals adopt smartphones, using digital wallets to facilitate payments has become increasingly popular. Customers are drawn to the convenience of paying bills or making purchases with a simple tap of their devices. Digital payment platforms, such as Apple Pay, Google Wallet, and others, have simplified the way consumers conduct transactions. They enable users to link their bank accounts directly, allowing instant access to funds at their fingertips. Furthermore, the speed of these transactions reduces the time it takes to complete purchases, adding to the overall customer satisfaction. As digital wallets increasingly focus on user experience, banks are required to adapt their systems to cater to these evolving needs effectively. Integration with point-of-sale systems worldwide has led to new opportunities for retail and service industries, enhancing the revenue landscape. Additionally, businesses can choose to offer exclusive promotions or loyalty programs through these wallets, encouraging consumer engagement. The synergy created between consumers and retailers through digital wallets benefits the entire ecosystem, showcasing a positive shift in banking interactions.

Security features in digital wallets have become a crucial aspect of their design and functionality. As users store sensitive information such as credit card numbers or identification data within these applications, security risks often arise. Banks and tech companies are continually investing in state-of-the-art encryption and fraud detection technology to protect their clients. Measures like biometric verification and two-factor authentication are becoming standard to fortify security protocols. Such advancements reassure users that their information is safeguarded, allowing for a more comfortable banking environment. Furthermore, users have increasingly expressed concern over data privacy, prompting financial institutions to adopt transparent policies surrounding the handling of personal information. Ensuring that digital wallets comply with regulatory standards is vital for maintaining trust between consumers and service providers. Addressing these security challenges not only protects users but also fulfills a legal responsibility for banks and tech companies. As these platforms continue to evolve, enhanced security features will remain key to driving adoption rates. In summary, a strong focus on security will guarantee sustained growth and consumer confidence in digital wallet technologies.

The Future of Digital Wallets in Banking

The future of digital wallets in banking looks promising, with new developments on the horizon. As technology evolves, financial institutions will likely adapt their services to incorporate artificial intelligence and machine learning. These innovations can help digital wallets process transactions more intelligently, learning user behavior to enhance the overall experience. Additionally, integrating advanced analytics will further enable banks to offer personalized services, tailored to individual customer needs. Financial establishments might even partner with fintech companies to develop cutting-edge wallet applications, maintaining a competitive edge in the industry. Furthermore, as cryptocurrencies gain traction, digital wallets are positioned to support such transactions, enabling customers to manage multiple types of currencies easily. This compatibility will significantly alter consumer perceptions of traditional banking, amplifying the relevance of financial institutions in this changing landscape. Moreover, regulatory adjustments will play a pivotal role in shaping the future of digital wallets. Policymakers may introduce new guidelines promoting interoperability, which will enable users to transfer funds across different digital platforms seamlessly. As we look ahead, the adoption of digital wallets in banking will ultimately redefine transaction methods and behaviors for consumers worldwide.

The impact of digital wallets extends beyond consumer convenience, influencing financial inclusivity as well. Digital wallets can help bridge the gap for unbanked individuals by providing a platform to access essential financial services. Rather than relying on traditional financial institutions, users can deposit cash into their digital wallets without requiring a bank account. This ability can significantly assist populations lacking traditional banking access in developing regions. Furthermore, digital wallets often come with low transaction fees compared to conventional banking solutions, making them a more financially viable option for users. This democratization of financial services could empower low-income communities, promoting savings and facilitating transactions. Local businesses can also benefit from the integration of digital wallets, as they facilitate smoother transactions and improved cash flow. By lowering barriers to entry, digital wallets can promote entrepreneurship and economic development in underserved areas. As these platforms continue to see increased adoption rates, the potential for economic growth and financial equality becomes more apparent. Ultimately, digital wallets stand to reshape the future of banking for diverse demographics and communities around the globe.

Marketing strategies within banking are evolving alongside the rise of digital wallets, necessitating a shift in approach. Banks need to rethink their methods of engaging customers by utilizing data and analytics derived from digital wallet transactions. Understanding customer preferences and behavior allows financial institutions to tailor their marketing efforts more effectively. Personalized marketing can empower banks to offer targeted promotions and incentives, driving user engagement with their digital wallet platforms. Additionally, collaboration with technology firms can result in innovative marketing campaigns that showcase unique capabilities of these wallets. Furthermore, banks can leverage social media to educate consumers on the benefits of using digital wallets, influencing adoption rates. The importance of user experience cannot be overstated; banks that prioritize intuitive design and functionality are likely to gain a competitive edge. As part of this marketing strategy, financial institutions should emphasize the security aspects of digital wallets and their ease of use. Overall, a comprehensive marketing approach centered on customer experience, technological innovation, and engagement will reinforce the growing presence of digital wallets in banking.

Challenges Facing Digital Wallet Adoption

Despite the many advantages of digital wallets, challenges remain in widespread adoption within the banking sector. One significant hurdle is the lack of standardization among various platforms, which can create confusion for users. Customers may find it challenging to navigate multiple digital wallets, each with unique features and functionalities, leading to frustration. Additionally, concerns surrounding security breaches can deter potential users from embracing this technology entirely. Incorporating user-friendly security measures is vital in addressing these concerns and fostering trust in digital wallets. Furthermore, regulatory compliance may present barriers to entry, as financial institutions must adhere to guidelines while innovating their wallet solutions. Socioeconomic factors also play a role in digital wallet adoption, particularly among older demographics who might be less inclined to adopt new technologies. To overcome these hurdles, extensive education and outreach programs are essential for raising awareness and understanding of digital wallets. As these challenges are addressed, financial institutions will be better positioned to harness the potential of digital wallets and reshape the landscape of banking transactions.

In conclusion, digital wallets have undeniably influenced banking transactions and transformed financial services. Their convenience, security, and innovative features appeal to consumers and businesses alike. As technology continues to evolve, banks must adapt to these changes by embracing digital wallet solutions. The potential for economic inclusion, personalized marketing, and enhanced security presents numerous opportunities for growth in the banking sector. However, facing challenges such as standardization and consumer awareness remains crucial for broader acceptance. Collaboration between banks, technology firms, and consumers will shape the future of digital wallets in banking. By overcoming existing barriers and implementing solutions, the financial industry can leverage digital wallets to improve customer experiences and redefine how we manage money. Furthermore, as we evolve towards a more cashless society, the importance of digital wallets will only increase. These innovative payment tools will continue to shape the way we think about financial transactions, enabling a more streamlined approach to managing finances. The journey of digital wallets from novelty to necessity highlights their significance in modern banking and finance.